“We are on the precipice of the greatest retirement crisis in the history of the world. And that makes perfect sense because, first of all, we have the largest elderly population in the history of the world.

Just focusing on the United States: our elderly are woefully unprepared to retire. And in the decades to come we will witness millions of elderly Americans, Baby Boomers and others, slipping into poverty. ‘Too frail to work, too poor to retire’ will become the new normal for many elderly Americans.”

So warns forensic pension analyst Ted Siedle.

And Ted knows what he’s talking about.

He’s a former SEC attorney who has testified on pension abuse before the Senate Banking Committee. And in 2017, he secured the largest SEC whistleblower award in history of $48 million, and in 2018, the largest CFTC award in history at $30 million.

Too many of America’s public pensions are dangerously underfunded due to over-promised payouts vs contributions and poor fund performance. And corporate pension funds are in the hole a collective -$50 billion.

ZIRP has pushed these funds out of conservative investments into highly risky and opaque instruments they have no business being in. And that the rosy case, assuming markets continue their current trajectory.

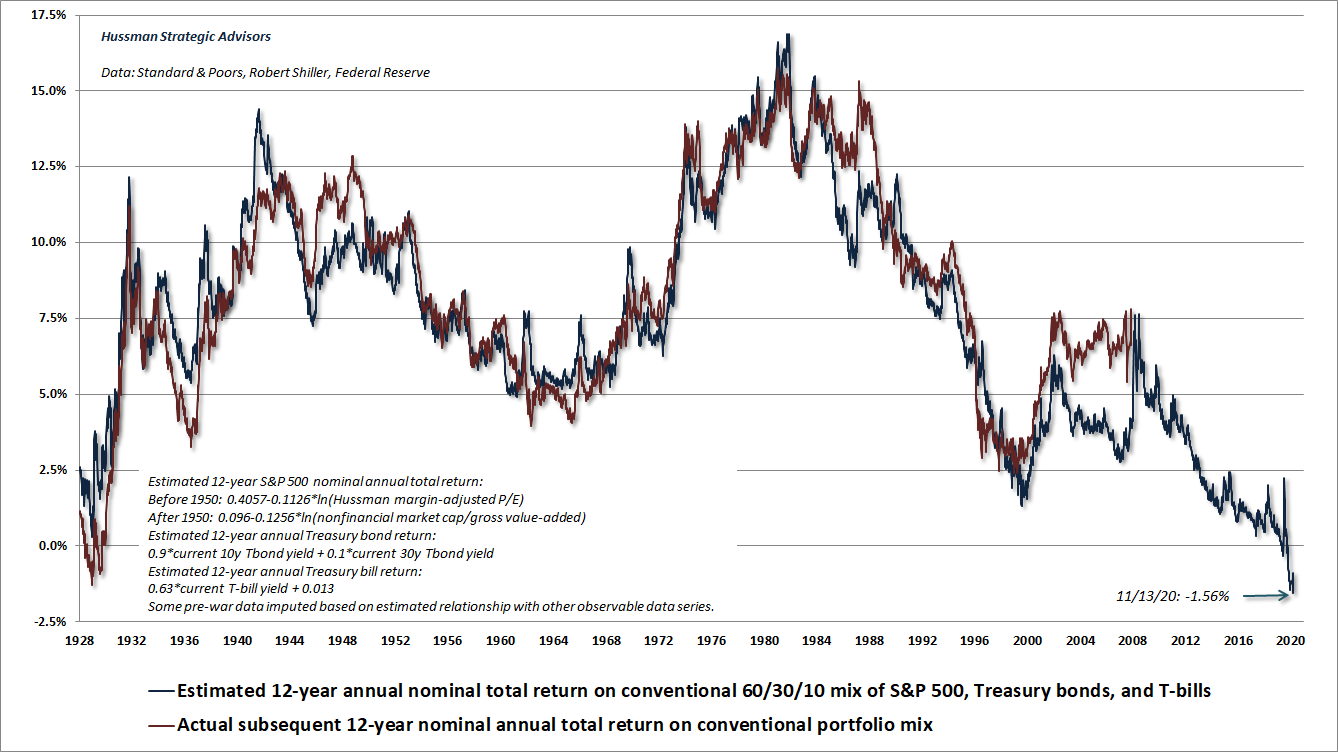

But given how overvalued they are, even just a period of 0% returns (which respectable analysts like John Hussman are waring will be the return over the next 12 years), let alone a sizable market correction, will unleash a catastrophic

by jrice2s

by jrice2s

{kind=link}