Many serious oil analysts, myself especially, thought that by now oil would have easily breached $200 a barrel. But it hasn’t, and it’s parked under $100, if you can believe that.

This Bloomberg article, which we’ll tear into together, provides perhaps the clearest explanation for why oil isn’t $200, and why it could easily smash to that level – and higher – given the fragility of the Middle East ‘ceasefire’ and rapidly dwindling oil reserves.

Twice a week, on Monday and Friday, I cover a round-up of all the news that you need to know and put it into a publication for subscribers, I call The Fat Pipe. I spend dozens of hours scanning and then assembling all the news that a well-informed person needs to know in order to remain properly oriented to world events, and to make better decisions about big, important things like protecting one’s wealth and preparing for the future and whatever may come.

This past weekend, June 6th and 7th, more missiles and bombs flew between Iran and Israel. Before they did, Trump told reporters that “he calls the shots” and that Bibi Netanyahu “won’t have any choice” but to keep the peace with Iran.

But Israel then immediately bombed Beirut, prompting Iran to lob ~ 10 missiles at Israel.

In response, Trump demanded that both sides immediately stop shooting and claimed, for what felt like the millionth time, that the peace deal was actually proceeding along well and would soon be completed.

In other words, typical pre-market Monday morning words meant to soothe the markets.

Oil, for its part, nudged up a couple of dollars upon the news of the war resuming, but then mostly gave up those gains again upon hearing the soothing words.

What gives? In times past, events far smaller than those of the past few weeks would have sent oil soaring into the stratosphere.

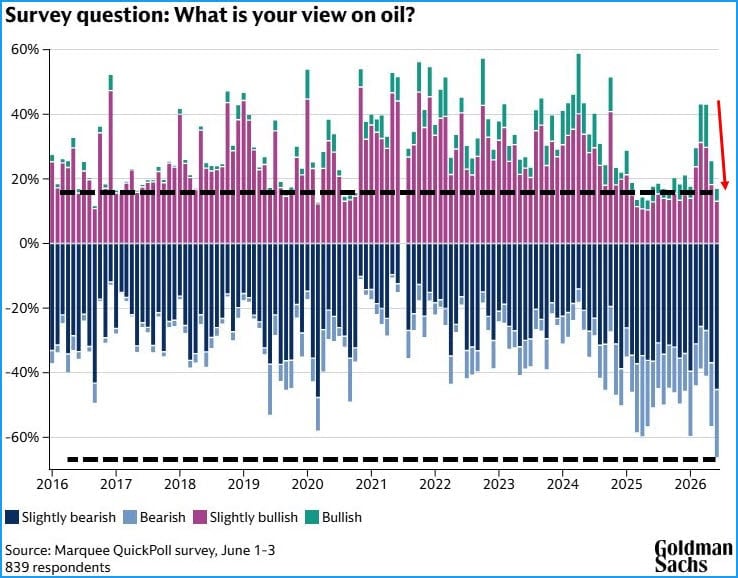

Things are so weird that, according to a Goldman Sachs survey, oil traders are more bearish on the price of oil than at any time over the past ten years.

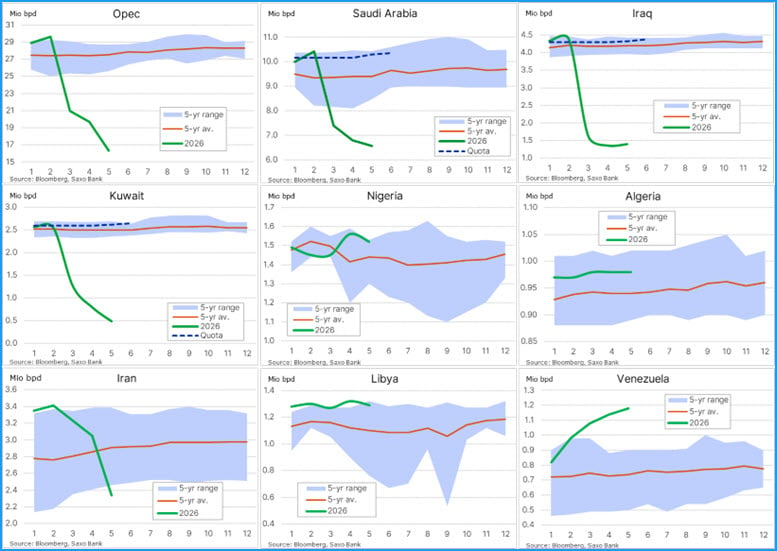

And their bullishness is plumbing 10-year lows. How can this be? How can oil traders be more bearish and the most weakly bullish they’ve been despite these clearly alarming charts of lost oil production?

Note that the scales are different on all the left axes. The loss of ~10 Mb/d from OPEC is not even modestly offset by Venezuela’s increase of 0.4 Mb/d.

Returning to the Bloomberg article, beginning with the opening paragraphs:

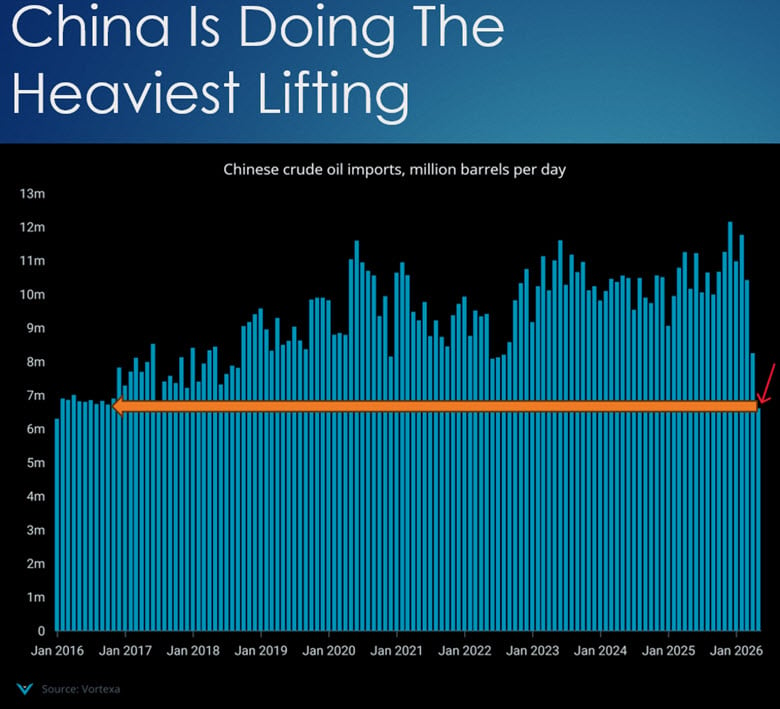

Oil’s price has been held back by a combination of factors; record US exports and a truly stunning collapse of Chinese imports which are down roughly 4 million barrels per day (Mb/d) in May.

This is per China’s wishes. It is a deliberate decision to sacrifice its own stockpiles vs attempting to import enough oil for its own domestic needs.

So that has cushioned the blow by 4 Mb/d.

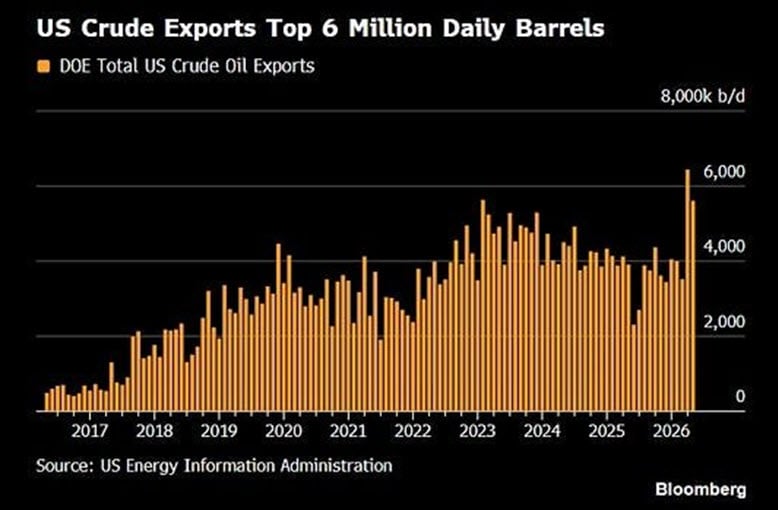

Another 2 Mb/d cushion has come from US exports.

As we’ve established previously, many times, the US is a net oil importer, not exporter, to the tune of about 2.3 Mb/d. Which means that for the US to be exporting 2 Mb/d more oil it must be eating into reserves and stockpiles, which, indeed, it is.

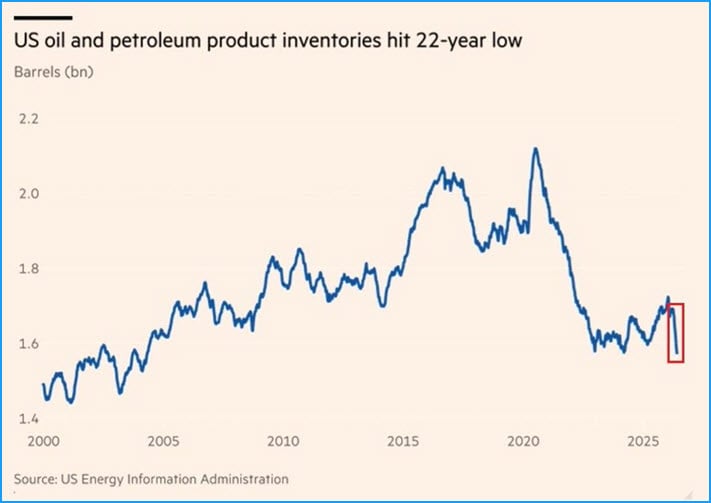

With the Iran war having passed the 100-day mark, and without any apparent desire on the part of Israel or the US to bring the war to a negotiated conclusion, we’re left with the idea that the Strait of Hormuz will remain closed indefinitely.

Coupled with the fact that the US and China are busy holding the price of oil down, which leads to far higher demand upon existing but dwindling oil stocks, it means we’re going to just keep on doing this until we smash into true shortages and market chaos.

One last quote set from the Bloomberg article:

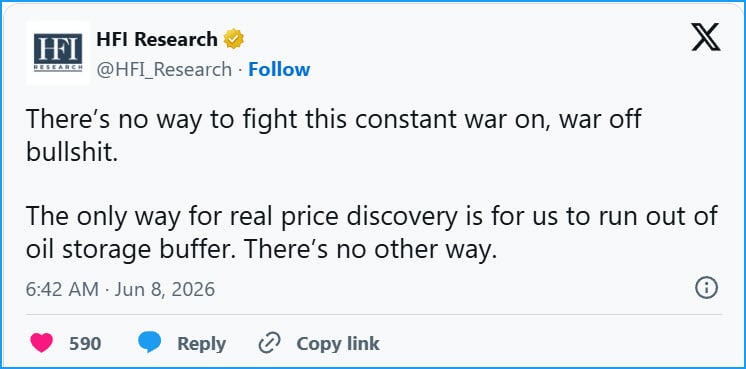

If we’re not capable of sustaining exports at these levels, but we’re also not meaningfully progressing towards a durable ceasefire, and at the same time, oil prices cannot rise for some reason, how exactly does US leadership think this will all play out?

I think HFI research put it well this morning.

To which I might add, it didn’t have to be this way.

So we’re (by which I mean everybody in the world) streaming at high speed toward tank bottoms, and there’s nothing currently on the political table that might slow us down. Trump wants low oil prices, and he doesn’t want to concede anything ot Iran. It might not matter anyway because Israel is clearly going to do what it feels is in its best interests and ignore Trump’s pleas for restraint.

Oil demand will remain too high for the circumstances, and all parties involved will draw down their precious reserves until a true panic sets in. How long before that happens? It could be a couple of months, but speaking rationally, countries should already be limiting oil use and hoarding what they can for themselves. But politics and markets are rarely rational, so here we are, and here we go.

by cmartenson

by cmartenson